Do you want to become data scientist?

Do you want to become a data scientist and pursue a lucrative career with a high salary, working from anywhere in the world? I have developed a unique course based on my 10+ years of teaching experience in this area. The course offers the following:

- • Learn all the basics of data science (value $10k+)

- • Get premium mentoring (value at $1k/hour)

- • We apply to jobs for you and we help you land a job, by preparing you for interviews (value at $50k+ per year)

- • We provide a satisfaction guarantee!

If you want to learn more book a call with my team now or get in touch.

Regression algorithms in Scikit-Learn

Regression is a robust statistical measurement for investigating the relationship between one or more independent (input features) variables and one dependent variable (output). In AI, regression is a supervised machine learning algorithm that can predict continuous numeric values. In simpler words, input features from the dataset are fed into the machine learning regression algorithm, which predicts the output values.

In this post, we’ll share a machine learning algorithms list of prominent regression techniques and discuss how supervised regression is implemented using the scikit-learn library.

Linear Regression

Linear regression is a machine learning algorithm that determines a linear relationship between one or more independent variables and a single dependent variable to predict the most suitable value of the dependent variable by estimating the coefficients of the linear equation.

The following straight-line equation defines a simple linear regression model that estimates the best fit linear line between a dependent (y) and an independent variable (x).

y=mx+c+e

The regression coefficient (m) denotes how much we expect y to change as x increases or decreases. The regression model finds the optimal values of intercept (c) and regression coefficient (m) such that the error (e) is minimized.

In machine learning, we use the ordinary least square method, a type of linear regression that can handle multiple input variables by minimizing the error between the actual value of y and the predicted value of y.

The following code snippet implements linear regression using the scikit-learn library:

# Import libraries import numpy as np from sklearn.linear_model import LinearRegression # Prepare input data # X represents independent variables X = np.array([[1, 1], [1, 2], [1, 3], [2, 1], [2, 2], [2, 3]]) # Regression equation: y = 1 * x_0 + 2 * x_1 + 3 # y represents dependant variable y = np.dot(X, np.array([1, 2])) + 3 # array([ 6, 8, 10, 7, 9, 11]) reg = LinearRegression().fit(X, y) reg.score(X, y) # Regression coefficients reg.coef_ # array([1., 2.]) reg.intercept_ # 2.999999999999999 reg.predict(np.array([[4, 4]])) # array([15.]) reg.predict(np.array([[6, 7]])) array([23.])

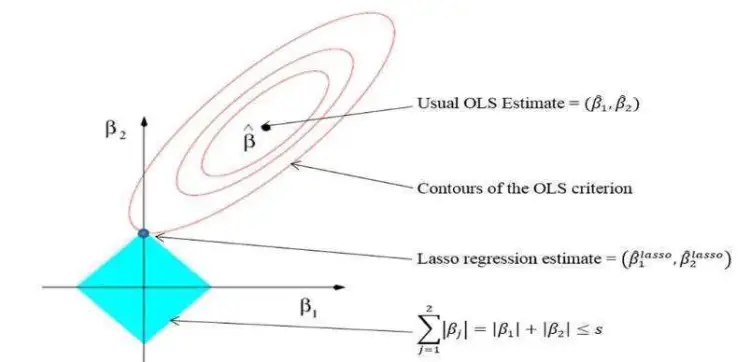

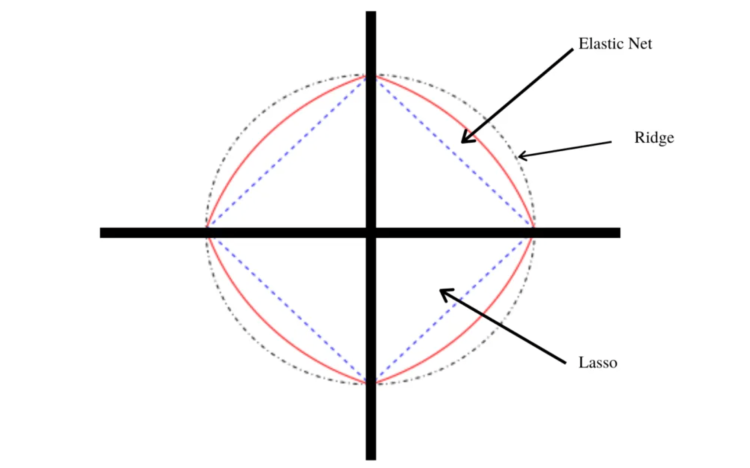

Lasso Regression–Least Absolute Shrinkage and Selection Operator

Linear regression can overestimate regression coefficients, adding more complexity to the machine learning model. The model becomes unstable, large, and significantly sensitive to input variables.

LASSO regression is an extension of linear regression that adds a penalty (L1) to the loss function during model training to restrict (or shrink) the values of the regression coefficients. This process is known as L1 regularization.

L1 regularization shrinks the values of regression coefficients for input features that do not make significant contributions to the prediction task. It brings the values of such coefficient down to zero and removes corresponding input variables from the regression equation, encouraging a simpler regression model.

The following code snippet shows how scikit-learn implements lasso regression in Python. In scikit-learn, the L1 penalty is controlled by changing the value of alpha hyperparameter (tunable parameters in machine learning which can improve the model performance).

# Import library from sklearn import linear_model # Building lasso regression model with hyperparameter alpha = 0.1 clf = linear_model.Lasso(alpha=0.1) # Prepare input data X = np.array([[1, 1], [1, 2], [1, 3], [2, 1], [2, 2], [2, 3]]) y = [ 6, 8, 10, 7, 9, 11] clf.fit([[0,0], [1, 1], [2, 2]], [0, 1, 2]) # Regression coefficients clf.coef_ # array([0.6 , 1.85]) clf.intercept_ # 3.8999999999999995 clf.predict(np.array([[4, 4]])) # array([13.7]) clf.predict(np.array([[6, 7]])) # array([20.45])

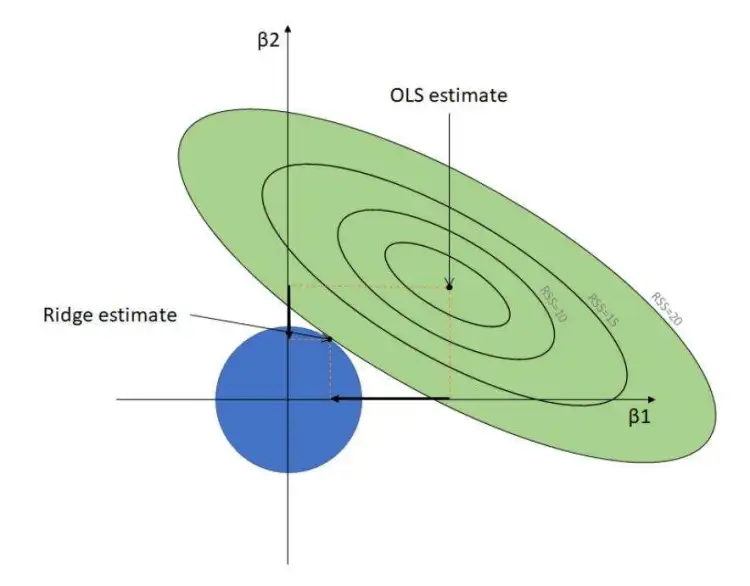

The Ridge Regression Algorithm

Ridge regression is another regularized machine learning algorithm that adds an L2 regularization penalty to the loss function during the model training phase. Like lasso, ridge regression also minimizes multicollinearity, which occurs when multiple independent variables show a high correlation with each other.

L2 regularization deals with multicollinearity by minimizing the effects of such independent variables, reducing the values of corresponding regression coefficients close to zero. Unlike L1 regularization, it prevents the complete removal of any variable.

The following code snippet implements ridge regression using the scikit-learn library. In scikit-learn, the L2 penalty is weighted by the alpha hyperparameter.

# Import library from sklearn.linear_model import Ridge # Building ridge regression model with hyperparameter alpha = 0.1 clf = Ridge(alpha=0.1) # Prepare input data X = np.array([[1, 1], [1, 2], [1, 3], [2, 1], [2, 2], [2, 3]]) y = [ 6, 8, 10, 7, 9, 11] clf.fit(X, y) clf.coef_ # array([0.9375, 1.95121951]) clf.intercept_ # 3.1913109756097553 clf.predict(np.array([[4, 4]])) # array([14.74618902]) clf.predict(np.array([[6, 7]])) # array([22.47484756])

The Elastic Net Regression Algorithm

Elastic net regression is a regularized linear regression algorithm that linearly combines both L1 and L2 penalties and adds them to the loss function during the training process. It balances lasso and ridge regression by assigning appropriate weight to each penalty, improving model performance.

Elastic net has two tunable hyperparameters, i.e., alpha and lambda. Alpha determines the percentage of weight given to each penalty, while lambda governs the percentage of the weighted sum of both penalties that contribute towards model performance.

The following code snippet demonstrates elastic net regression using scikit-learn:

# Import library from sklearn.linear_model import ElasticNet # Building elastic net regression model with hyperparameter alpha = 0.1 regr = ElasticNet(alpha=0.1) # Prepare input data X = np.array([[1, 1], [1, 2], [1, 3], [2, 1], [2, 2], [2, 3]]) y = [ 6, 8, 10, 7, 9, 11] regr.fit(X, y) regr.coef_ # array([0.66666667, 1.79069767]) regr.intercept_) # 3.9186046511627914 regr.predict([[4, 4]]) # array([13.74806202]) regr.predict([[0, 0]]) # array([20.45348837])

Regression Can Handle Linear Dependencies

Regression is a robust technique for predicting numerical values. The machine learning algorithms list provided above contains powerful regression algorithms that can conduct regression analysis and prediction for various machine learning tasks using the scikit-learn Python library.

However, regression is more suitable when the dataset contains linear relationships among dependent and independent features. To handle non-linear dependencies among data features other regression algorithms, such as neural networks are used as they can capture non-linearities using activation functions.

If you want to pursue a career in data science, check out our webinar on what it’s like to be a data scientist, and check my new program Beyond Machine! And if you have any queries regarding this post, get in touch with us.

If you want to pursue a career in data science, check out our webinar on what it’s like to be a data scientist, and check my new program Beyond Machine and Masters in Machine learning! And if you have any queries regarding this post, get in touch with us.

Do you want to become data scientist?

Do you want to become a data scientist and pursue a lucrative career with a high salary, working from anywhere in the world? I have developed a unique course based on my 10+ years of teaching experience in this area. The course offers the following:

- • Learn all the basics of data science (value $10k+)

- • Get premium mentoring (value at $1k/hour)

- • We apply to jobs for you and we help you land a job, by preparing you for interviews (value at $50k+ per year)

- • We provide a satisfaction guarantee!

If you want to learn more book a call with my team now or get in touch.